Sunday, February 05, 2006

Shooting For Average : Index funds in your portfolio

Index funds are well-known for their advantages: low expenses, passive management, and, in most cases, zero loads. Index funds shoot for average performance at low cost. While most index funds in the US track broad indices, such as the S&P500 or the Wilshire 5000, Indian index funds track either the 30-stock Sensex or the 50-stock Nifty. These narrow indices represent the bluest of the Indian blue-chips but are too small to represent the entire market. My argument is that, given these narrow indices, an investor should look at index funds as the replacement of the large-cap part of his or her portfolio.

Lake Wobegon

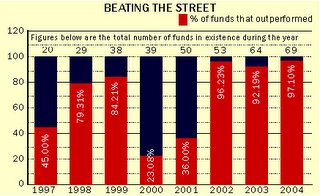

Figure 1 shows the number of funds outperforming the Sensex each year since 1997. If 90% of mutual funds can outperform the Sensex for three years running, the Sensex is not the average. Either that, or we have the change the definition of average.

Figure 1: >90% MFs beat the Sensex in 2002-2004

Looking at the best-performing mutual funds for the trailing year shown in Table 1, we can see that the average large-cap holding of the mutual funds is 38.20% and that the average capitalization of the companies in the portfolio is ~Rs.5000Cr. Compare this with the average capitalization of the index stocks of Rs30,000Cr (Sensex) and Rs.27,000Cr (Nifty). The average capitalization of the companies that these funds invest in is less than 1/5th of that of the index stocks.

FUND NAME | Average Market Cap (Rs.Cr) | % in Large Caps (2005) | 1-year returns(trailing) |

Sensex | ~33000 | 100.00% | 47.17 |

Nifty | ~27000 | 100.00% | 41.41 |

1249.28 | 8.00% | 80.21 | |

1219.11 | 5.00% | 86.78 | |

5088.72 | 50.00% | 83.24 | |

856.07 | 0.00% | 83.15 | |

5293.63 | 55.00% | 78.88 | |

3210.94 | 34.00% | 73.97 | |

7156.14 | 56.00% | 73.61 | |

7552.52 | 57.00% | 72.63 | |

5631.47 | 47.00% | 72.23 | |

14059.88 | 70.00% | 71.41 | |

Average | 5131.78 | 38.20% | 77.61 |

Table 1: Best performing funds (1-year trailing)

But what about active mutual funds that are fishing in the same pond as these indices? It would seem logical that, with the weight of professional management behind them, mutual funds investing in large-cap companies would outperform the indices. Table 2 shows the performance of mutual funds with the highest proportion of large caps in their portfolio.

| FUND NAME | Average Market Cap (Rs.Cr) | % in Large Caps (2005) | 1-year returns (trailing) |

| Sensex | ~33000 | 100.00% | 47.17 |

| Nifty | ~27000 | 100.00% | 41.41 |

| UTI Index Select Equity | 44817.79 | 95.00% | 42.43 |

| ING Vysya Nifty Plus | 40848.18 | 99.00% | 36.26 |

| Can D'Mat | 34529.66 | 100.00% | 62.51 |

| HDFC Index Sensex Plus | 32157.91 | 94.00% | 48.68 |

| LICMF Sensex Advantage | 31037.17 | 94.00% | 43.91 |

| UTI Large Cap | 27345.49 | 93.00% | 35.4 |

| DSPML Top 100 Equity | 27339.49 | 96.00% | 52.11 |

| UTI PSU | 24023.05 | 85.00% | 31.5 |

| BirlaSun Life Frontline Equity | 22355.76 | 79.00% | 49.12 |

| Cangrowth Plus | 21769.13 | 84.00% | 59.6 |

| Average | 30622.36 | 91.90% | 46.15 |

Table 2: Large-cap mutual funds (1-year trailing)

Using an index fund

If an investor just chooses the funds with the best past returns, he or she will be overweight on small-cap and mid-caps stocks. An approach that could work is to take care of the large-cap representation with an index fund first. This leaves the investor free to choose a basket of funds that invest exclusively in small-caps and mid-caps to top off the portfolio.

Friday, February 03, 2006

Reading The Signs: What does a good mutual fund look like?

This post came about because of my doubts about the performance of index funds in India. Index funds in the US routinely outperform the majority of actively-managed funds. The theory is that long-term returns of most funds will be the average market return minus incurred costs of investment. So, passive index funds outperform active funds over the long-term by the sizeable difference in expenses. With respect to India, questions that I cannot answer for now are:

- Do the narrow sensex and nifty represent the market? If they don't, that's one assumption down.

- What are the long-term returns of mutual funds here? The lack of history of mutual funds is a problem here.

- What are the long-term returns of the indices with dividends reinvested (the so-called total return) and how do they compare with active funds? all sorts of information availability issues.

- How is one to know how to rate a mutual fund?

- How can we pick a mutual fund that has the highest chance of good (and consistent) returns?

- What if the fund manager quits, bets heavily on sectors or follows the market hype?

Here's my list.

#1 Small Size

This is not a small-cap versus big-cap argument. A small mutual fund invested in large-caps is just as safe (or risky) as a large mutual fund of the same class. The argument here is that a fund manager with smaller assets under management (AUM) will be able to better manage his or her portfolio. Further, a fund manager with a small AUM needs smaller winners than a fund manager with a larger AUM. The bigger you get, the harder it is to beat the average (I have seen the average and it is us). As Warren Buffett is said to have remarked, 'I can double your money as long as it is less than a million dollars'. The nervousness of going against the crowd (Ex: if he/she's so good, how come they don't have a bigger fund?) can be ameliorated by examining the fund further.

#2 Low Expense Ratios

This is quite obvious. Expenses eat away at your returns. The lesser your fund spends, the more you get to keep.

#3 Low turnover

Turnover numbers indicate the rate at which the composition of a portfolio changes. A high turnover indicates that the fund manager is second-guessing himself or herself. If the manager has that little faith in their choices, why should you have any at all? The other explanation could be that the manager is a market timer and/or a follower of short-term trends.

#4 Consistent Methodology

If the fund manager shares your views on investment, that's a good beginning. Every fund says that they want to invest in stocks at fair values and shoot for long-term appreciation. No one is going to come out and say 'we're going to chase hot sectors all year

#5 Entry Loads

Entry loads are much the same as expense ratios. The lower, the better.

#6 Long-Term view

Can your fund say no? Some mutual funds chase short-term returns to increase their assets under management or preserve their existing assets since investor flee at the first hint of underperformance. This pressure on short-term returns puts existing investors at risk for the benefit of the manager or the fund. If the fund had a long-term view, it would drive short-termers away and leave the ones that share the manager's views (This is a good thing).

#7 Consistent Returns

Obviously, a consistent above-average return is good. The manager must be doing something right. Just as important as the returns is the means by which they were obtained. A fund with many good performers is much better than a fund with a few rockets and a lot of duds. The manager is showing consistently good judgement in the former case.

This is not a condition for a mutual fund to do well but it should be the ONLY way you must invest in mutual funds. This is the first sieve I'd use. No SIP, no way.

Choosing a good mutual fund is the beginning. Keeping tabs on the fund with respect to the above is what is going to really get to you. Enough to make me wish index funds work.

![]()